Diagnostics for GLMs

How does one find outliers, influential

observations?

How about prediction intervals, confidence

intervals?

https://www.sagepub.com/sites/default/files/upm-binaries/21121_Chapter_15.pdf

[Textbook]

Leverage Score

Estimation

https://icml.cc/2012/papers/80.pdf [2012

Fast approximation of matrix coherence and statistical leverage]

Firstly, we have to derive the hat matrix

for GLMs. We find that:

|

|

Also notice the sum of the leverage scores is equal to the number

of parameters in the model.

[BE CAREFUL NOT ALWAYS!!! Ie like in

Ridge Regression]

However

be careful! The TRUE hat matrix is NOT the formula above, but rather:

|

|

Ive

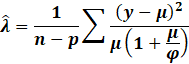

confirmed the norm between them is off by around p - rank(H).

However, since we only want the leverage scores, we use the trace

property cycling property.

|

|

However, on further notice, we notice via the Cholesky

Decomposition that:

|

|

All in all, this optimized routine computes both the

variances(beta) and leverage(X) optimally in around:

np^2 + 1/3p^3 + 1/2p^3 + p^2 + np^2 + np + n FLOPS.

Or around:

(2/3)p^3 + (2n)p^2 + (n+1)p FLOPS.

And peak memory consumption:

n/Bp + p^2 + n + p SPACE.

Where B is the batch size.

Now going about estimating the leverage scores or the diagonal hat

matrix is a pain. One clearly will be crazy on computing

the full hat matrix then only extracting the diagonals.

Instead sketching comes to the rescue again!

|

|

Also notice the maximum leverage score must be 1 [leverage scores

are between 0 and 1.]

Also, notice the scaling of the normal distribution sketch.

Now the sketching matrices can be the count sketch matrix.

S2 should NOT be a count sketch matrix, since during the

triangular solve.

Notice the error rate. That means in general if the sketching size

requires too many observations,

you would rather use the original matrix.

Standardized,

Studentized Residuals

Pearson residuals are

the per observation component of the Pearson goodness of fit test ie:

|

|

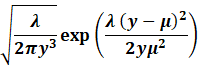

Where we have for the exponential family:

|

Name |

Distribution |

Range |

|

|

|

Poisson |

|

|

|

|

|

Quasi Poisson |

|

|

|

|

|

Gamma |

|

|

|

|

|

Bernoulli |

|

|

|

|

|

Inverse Gaussian |

|

|

|

|

|

Negative

Binomial |

|

|

|

|

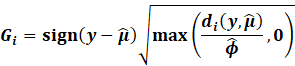

Standardized Pearson Residuals

then correct for the leverage scores:

[These are also called internally studentized residuals]

|

|

For practical models:

|

Name |

Range |

|

|

|

|

Poisson |

|

|

|

|

|

Quasi Poisson |

|

|

|

|

|

Linear |

|

|

|

|

|

Log Linear |

|

|

|

|

|

ReLU Linear |

|

|

|

|

|

CLogLog Logistic |

|

|

|

|

|

Logistic |

|

|

|

|

The PRESS residuals showcase the difference in the

prediction and true value if we

excluded the observation from the model.

These can be proved by using the Sherman Morrison Inverse

Identity formula.

|

|

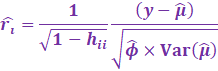

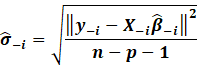

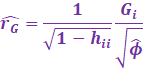

However, in outlier analysis, one generally considers the externally

studentized residuals,

which essentially is when the variance is estimated whenever each

observation is deleted it.

Minus 1 because one datapoint is deleted each time.

|

|

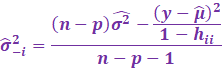

Now to simplify this, we utilize the PRESS residuals:

[ Gray part skips steps which are a bit tedious to showcase 😊 ]

|

|

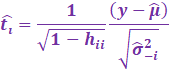

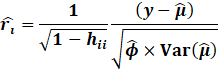

Then the externally studentized residuals utilises this new

excluded variance:

|

|

However in GLMs, we cannot resort to this estimate for the OLS

model.

Rather, we first remember the Deviance Residuals:

|

|

The standardized deviance residuals are then:

|

|

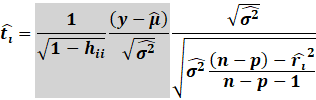

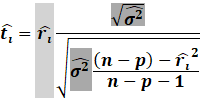

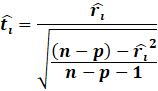

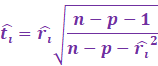

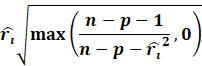

Then, we get the Williams approximation to externally

studentized residuals:

|

|

Which we find that:

|

|

For practical models:

|

Name |

|

|

|

|

|

Poisson |

|

|

|

|

|

Quasi Poisson |

|

|

|

|

|

Linear |

|

|

|

|

|

Log Linear |

|

|

|

|

|

ReLU Linear |

|

|

|

|

|

|

|

|

|

|

|

Logistic |

|

|

|

|

Cooks Distance,

DFFITS

Popular methods to detect influential or possible outliers include

the Cooks Distance and DFFITS.

|

|

The Cooks Distance is essentially the total change in MSE if an

observation is removed.

It shows how much error can be seen in standard deviation units on

how the error changes

if an observation is removed.

|

|

First notice by using the Sherman Morrison inverse formula that:

|

|

We then expand:

|

|

Generally, a cutoff of 4/n is reasonable. Likewise, one can use

the 50% percentile of the F distribution.

Though for large n, this will converge to 1.

On the other hand, DFFITS is a similar measure to the Cooks

Distance.

DFFITS rather uses the externally studentized residual, which is

more preferred than the Cooks Distance.

|

|

In fact, DFFITS is closely related to the Cooks Distance:

|

|

The cutoff value for DFFITS is:

|

|

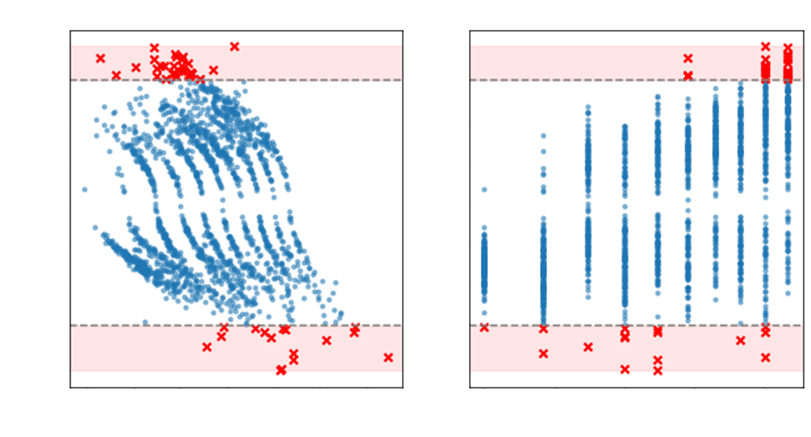

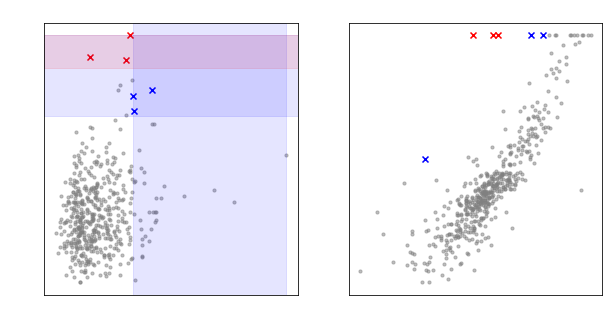

Finally to plot and showcase the possible outliers, one can use

for both axes:

|

|

However in practice, the identification of outliers is more

complicated than using DFFITS, since DFFITS can suggest

too many outlier candidates. Rather we use the Studentized

Residuals vs Leverage plot:

The cutoff is 3 * the studentized residual (ie the residual is 3

standard deviations away from the mean).

Likewise the leverage much be at least 2 times the average

leverage.

|

|

However, we need to also capture wildly off-putting results. So, we

also include anything above 5 standard deviations.

|

|

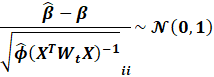

Confidence,

Prediction Intervals

Confidence and Prediction Intervals for both new data and old data

are super important aspects.

The trick is one utilises the leverage scores.

Remember that:

|

|

This essentially means that:

|

|

Notice how this is NOT the leverage

score!!!!!!

And then for GLMs, via the inverse link function (the activation

function):

|

|

Then, we have the upper

(97.5%) and lower (2.5%) confidence

intervals:

|

|

Be careful! Its the upper

(97.5%) and lower (2.5%) confidence

intervals! Not 95%.

For new data points though, we have to estimate the factor. We can

do this via:

[Where A is the new data matrix, psi is the new predicted value

and z is the new weight]

|

|

Remember though previously we performed the Cholesky Decomposition

on the variance matrix.

So, we can speed things up by noticing:

[Notice we exclude the new weights]

|

|

For Prediction Intervals, we shall not prove why, but there is in

fact a +1 factor inside the leverage square root:

|

|

Notice if the dispersion parameter is 1 (Poisson, Bernoulli

models), then the normal distribution is

used instead of the Student T distribution for the critical

values.

Copyright Daniel Han 2024. Check out Unsloth!